How green bonds can bolster the transition towards a more sustainable future

Samenvatting

The channelling of capital flows towards projects with measurable environmental benefits and tangible positive impacts on the energy transition marks a fundamental milestone in the transformational process of a global economy still largely dependent on finite resources to a sustainable- and clean-energy society. In this context, green bonds are an important vehicle to mobilise capital markets towards this green transition, as their use of proceeds is explicitly dedicated to projects with environmental benefits focusing on climate change mitigation and/or adaptation.

Samy Lounis

Fixed Income Product Specialist

The particularities of green bonds

As defined by the International Capital Markets Association1 in 2014, green bonds are “any type of bond instrument where the proceeds will be exclusively applied to finance or re-finance, in part or in full, new and/or existing eligible green projects and which are aligned with the four core components of the Green Bond Principles:”

- Use of Proceeds (identification of ‘green’ projects and assets)

- Evaluation and selection of eligible green projects

- Management of Proceeds (tracking, allocation and spending of proceeds)

- Reporting (what information to disclose, as well as the frequency of disclosure to investors, including methodologies for CO₂ emissions calculation).

Examples of eligible Green Bonds projects

*Information & communications technology

Source: Allianz Global Investors, Climate Bonds Initiative. For illustrative purposes only.

More precisely, green bonds differ from regular bonds solely in their “mission”, i.e., to apply investment proceeds to finance defined green projects.

A brief history of green bonds

With the issuance of the Climate Awareness Bond (CAB) in 2007,2 the European Investment Bank gave birth to the world’s first green bond. This marked the starting point of an unprecedented success story, gradually attracting a growing number of climate-conscious investors wishing to participate in growth prospects, whilst contributing to positive impact on energy and climate transition.

- 2007: First green bond issued by EIB

- 2008: World Bank issues its first green bond

- 2010: IFC issues its first green bond

- 2013: First corporate green bond (Vasakronan, a Swedish property company). First USD 1 billion green bond issued by IFC

- 2014: ICMA launches the Green Bond Principles, a set of voluntary guidelines for issuing Green Bonds, recommending transparency and disclosure. First green bond indices are created (BofAML, MSCI Barclays, S&P, Solactive)

- 2015: The Agricultural Bank of China issues the first GB from a Chinese bank, with a USD 1 billion dual currency bond (USD and Yuan)

- 2016: First sovereign green bond issued by Poland

- 2017: : First sovereign issuance from France, largest issue to date. New issues for 2017 exceed the USD 100 billion threshold for the first time (159 billion)

- 2018: EU announces its Sustainable Finance Action Plan

- 2020: More than USD 1 trillion green bonds have been issued since 2007

First issuance from Germany

Publication of the EU Taxonomy regulation. The EU Taxonomy is a green classification system that translates the EU’s climate and environmental objectives into criteria for specific economic activities for investment purposes. - 2021: First issuance from the European Union, the first of a massive green bond program of EUR 250 billion in the context of the Next Generation EU Recovery fund, which should turn the EU into the world’s largest green-bond issuer

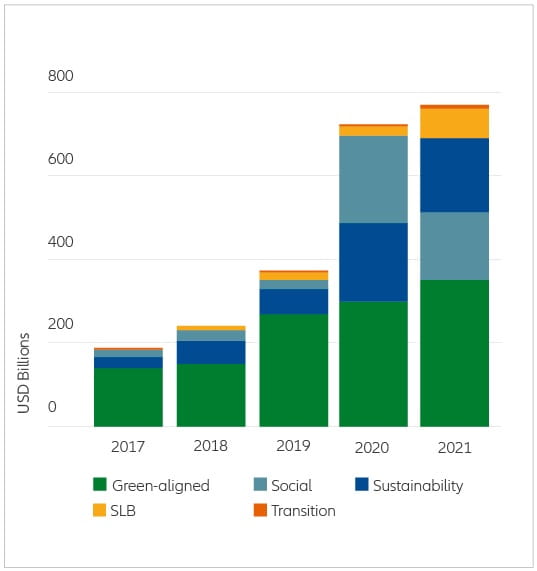

Since then, the climate-related multi-currency debt market has gained tremendous momentum.

According to recent reports, in the first three quarters of 2021 alone, the issuance of Green, Social and Sustainability, Transition and Sustainability-linked Bonds reached the USD 767.5 billion mark, with COP26 (and related expectations) serving as a catalyst. Recent analyst forecasts suggest that new issuance should continue to grow, going beyond even the USD 1 trillion mark in 2022.

Green bonds, a global success model

On a worldwide scale, green bonds have proven to be a multifaceted model for success, attracting a growing number of investors seeking sustainable, low-carbon investment opportunities. Their issuance reached over USD 450 billion in 2021, and is targeting the milestone of USD 1 trillion in 2023.3

With a better understanding of climate-change related challenges, with climate-change risks becoming more visible and measurable, and with tightening regulatory requirements and policies for sustainable investments, an increasing investor base is globally going “greener”.

Source: https://www.climatebonds.net/2021/11/2021-already-record-yeargreen-finance-over-350bn-issued

Source: https://www.climatebonds.net/resources/reports/sustainable-debt-summary-q3-2021

Can green bonds bridge the net zero emissions funding gap?

While climate-related issuance is growing globally, and green bonds issuance is reaching record levels, annual investment in the transition towards a net-zero emissions economy and society are still falling short.

According to the International Energy Agency, annual clean energy investment will need a threefold increase, and to arrive at approximately USD 4 trillion by 2030, to reach net zero emissions by 2050.4

Other estimates predict that over the next 15 years the cost arising from meeting climate pledges could amount to more than USD 90 trillion,5 while the annual global adaptation cost in a 2°C temperature rise scenario would be between USD 70 billion and USD 100 billion.6

The more divergent the different assessments of funding shortfalls might be, the more unanimous is the conviction that the annual investment required outstrips the ability of governments and public entities to finance it.

Therefore, green bonds of corporate issuers can help to mobilise additional capital, and to encourage the private sector to engage in the energy transition process.

AllianzGI powers the potential of key enablers of energy and climate transition

Allianz Global Investors identifies innovators that promote and shape the transition towards a sustainable- and cleanenergy economy and society, and which projects have a demonstrable and measurable positive impact on the environment. Allianz Global Investors invests for example in companies that have specialsed in developing large offshore wind farms, or in converting fossil-fuel powered power stations to run on biomass, or on other renewable energy materials/sources.

Those investments in pioneering renewable energy projects can be decisive contributions to avoiding a hundred thousand tons of CO2 emissions per year, and pave the way for a greener and more sustainable future.

1 https://www.icmagroup.org/assets/documents/Regulatory/Green-Bonds/Green-Bonds-Principles-June-2018-270520.pdf

2 https://www.eib.org/en/investor-relations/cab/index.htm

3 https://about.bnef.com/blog/sustainable-debt-issuance-hits-3-trillion-threshold/

4 https://www.iea.org/reports/net-zero-by-2050

5 https://www.weforum.org/agenda/2021/08/nine-steps-to-bridge-the-net-zero-funding-gap/

6 https://www.zawya.com/mena/en/projects/story/PROJECTS_INTERVIEW_Sustainabilitylinked_debt_market_to_bridge_climate_funding_gapZAWYA20211219072350/

Investing involves risk. The value of an investment and the income from it may fall as well as rise and investors might not get back the full amount

invested. Investing in fixed income instruments may expose investors to various risks, including but not limited to creditworthiness, interest rate, liquidity

and restricted flexibility risks. Changes to the economic environment and market conditions may affect these risks, resulting in an adverse effect to the

value of the investment. During periods of rising nominal interest rates, the values of fixed income instruments (including positions with respect to shortterm fixed income instruments) are generally expected to decline. Conversely, during periods of declining interest rates, the values of these instruments

are generally expected to rise. Liquidity risk may possibly delay or prevent account withdrawals or redemptions. Past performance does not predict

future returns. If the currency in which the past performance is displayed differs from the currency of the country in which the investor resides, then the

investor should be aware that due to the exchange rate fluctuations the performance shown may be higher or lower if converted into the investor’s local

currency. The views and opinions expressed herein, which are subject to change without notice, are those of the issuer companies at the time of

publication. The data used is derived from various sources, and assumed to be correct and reliable at the time of publication. The conditions of any

underlying offer or contract that may have been, or will be, made or concluded, shall prevail. The duplication, publication, or transmission of the

contents, irrespective of the form, is not permitted; except for the case of explicit permission by Allianz Global Investors GmbH.

For investors in Europe (ex. Switzerland)

This is a marketing communication issued by Allianz Global Investors GmbH, www.allianzgi.com, an investment company with limited liability, incorporated in Germany, with its registered office at Bockenheimer Landstrasse 42-44, 60323 Frankfurt/M, registered with the local court Frankfurt/M under HRB 9340, authorised by Bundesanstalt für Finanzdienstleistungsaufsicht (www.bafin.de). Allianz Global Investors GmbH has established branches in the United Kingdom, France, Italy, Spain, Luxembourg, Sweden, Belgium and the Netherlands. Contact details and information on the local regulation are available here (www.allianzgi.com/Info).

For investors in Switzerland

This is a marketing communication issued by Allianz Global Investors (Schweiz) AG, a 100% subsidiary of Allianz Global Investors GmbH.

2023994

Recente research

Don’t downsize your dreams

Is it time to revisit the UK as an asset class?

Samenvatting

UK equities have grown increasingly unloved over the past decade. Could that be about to change? A recent uptick in performance reminded investors what they are missing, and the market could offer growth and value opportunities.

Key takeaways

|